Cracking the Code on Telematics Insurance: My Takeaways from Insurance Innovators Nordics Summit

This week, I attended the Insurance Innovators Nordics Summit, where Verna was recognized as one of the top five InsurTechs in the region. In my pitch, I discussed why many telematics initiatives fail, despite 70% of customers being open to telematics insurance for lower premiums.

Fridrik Tor Snorrason

4/21/20232 min read

Earlier this week, I attended the excellent Insurance Innovators Nordics Summit where Verna was one of five companies that were selected as the brightest and best InsurTechs in the Nordic🚀

In my pitch, at the InsurTech evening on Monday, I identified a few rabbit holes that have caused most of the telematics initiatives to fail despite research showing that 70% of customers are willing to switch to telematics insurance if it lowers their premiums.

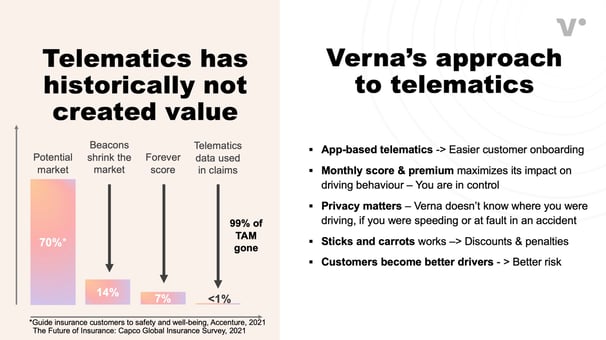

Mistake nr 1 - Asking the customers to install a beacon in their cars

One factor is insurers' insatiable appetite for data and accuracy. To satisfy it the insurers often ask customers to install beacons into their cars. This way the insurer can capture very detailed behavioral data about every single trip taken by the driver. The problem with this approach is it often produces a bad user experience but most customers can't simply be bothered with the hassle of installing them. The beacon approach has also caused significant privacy concerns.

Mistake nr. 2 - Creating a forever score

The second mistake is not thinking hard enough about how the score impacts the behavior of customers. A driving score that accumulates forever leaves customers with little incentive to improve their driving from one month to another.

Mistake nr. 3 - Using telematics data for claims

The third rabbit hole is the belief that since customers are willing to share telematics data to lower their premiums, they would also be happy to allow us to use the data in processing claims. A decision to use the telematics data for claims literally obliterates the potential market opportunity telematics insurance products offer. From a data privacy point of view, customers don‘t want insurers to have access to data which shows where they were driving, whether they were speeding or were at fault in an incident.

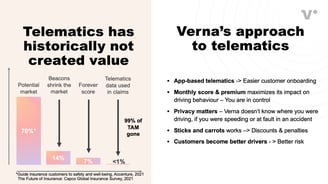

But does this mean we can't use telematics in insurance? Absolutely not. It simply means that you need to think much more carefully how to implement it in a way that provides the customer with a „fair data deal“ and a super user friendly solution.

It may sound counter intuitive to use the driving score only as a tool to influence the driving behavior of customers and to calculate monthly premiums. But this simplicity is much more likely to appeal to customers, which is a prerequisite for capturing the market opportunity that certainly is out there for the taking.

Finally, shoutout to the Insurance Innovators team and Plug and Play for organizing the InsurTech evening, and Tony Tarquini for moderating and guiding us through the evening. And congrats to Claims Carbon for taking home the InsturTech Evening's price.

This post was initially published on LinkedIn